A well-crafted investment portfolio is like a successful baseball team. Both consist of a diverse line-up of players, each of whom contributes in their own way across a long season.

Of course, in both sports and investing, you can’t tell the players without a scorecard. So, let’s get up close and personal with a couple of sluggers from the heart of the investing portfolio – growth stocks and value stocks. We’ll talk about the difference between growth stocks and value stocks and explore their respective career stats.

Growth stocks, as the name implies, are shares in companies that are expanding at a rapid pace. If, for example, corporate earnings are averaging 8%, a growth company might be at 12% or 20%. Some growth companies – including Amazon and Facebook — are seeking to dominate their industries. Others are pursuing less grandiose but still aggressive expansion plans. To fuel this kind of rocket ride, growth companies often need to reinvest all of their profits. As a result, growth stocks are less likely than other stocks to pay a dividend and rarely pay a high dividend percentage.

Investors buy growth stocks with the expectation those shares will experience significant price appreciation in the future. As a result, growth stock buyers typically pay higher multiples on those shares’ earnings. If the average stock is trading at a multiple of 15 times earnings, growth stocks might be trading at a 25 multiple.

Growth stocks are often found in the technology, discretionary spending, and healthcare sectors. Additional examples include Google, Visa, and Mastercard. The two credit card companies average a ½% dividend yield while Google, Facebook, and Amazon pay no dividends.

The above list of companies is purely for educational purposes and should not be considered any sort of recommendation.

Next in our portfolio line-up is value stocks.

Value stocks are shares in companies that are trading below what they may ultimately be worth based on a variety of financial metrics. Value stocks typically have low current price-to-earnings ratios and low price-to-book ratios. (Think of book value as the amount of money a company’s shareholders would receive if the business were liquidated.)

Investors buy value stocks hoping the shares will increase in price when the market recognizes the stock’s full potential. Using this classic “buy low, sell high” approach, value investors see the potential to make more money than if they had invested in higher-priced stocks that increased modestly in value.

Value stock companies are often mature, established leaders in their industries with lots of cash flow. The top sectors for value stocks include financial institutions, health care and industrials. Examples of value stocks include JP Morgan Chase (3% dividend yield), Exxon Mobil (5%), and Proctor & Gamble (2.3%).

Again, that list is for illustration purposes only and is not intended to be any sort of recommendation.

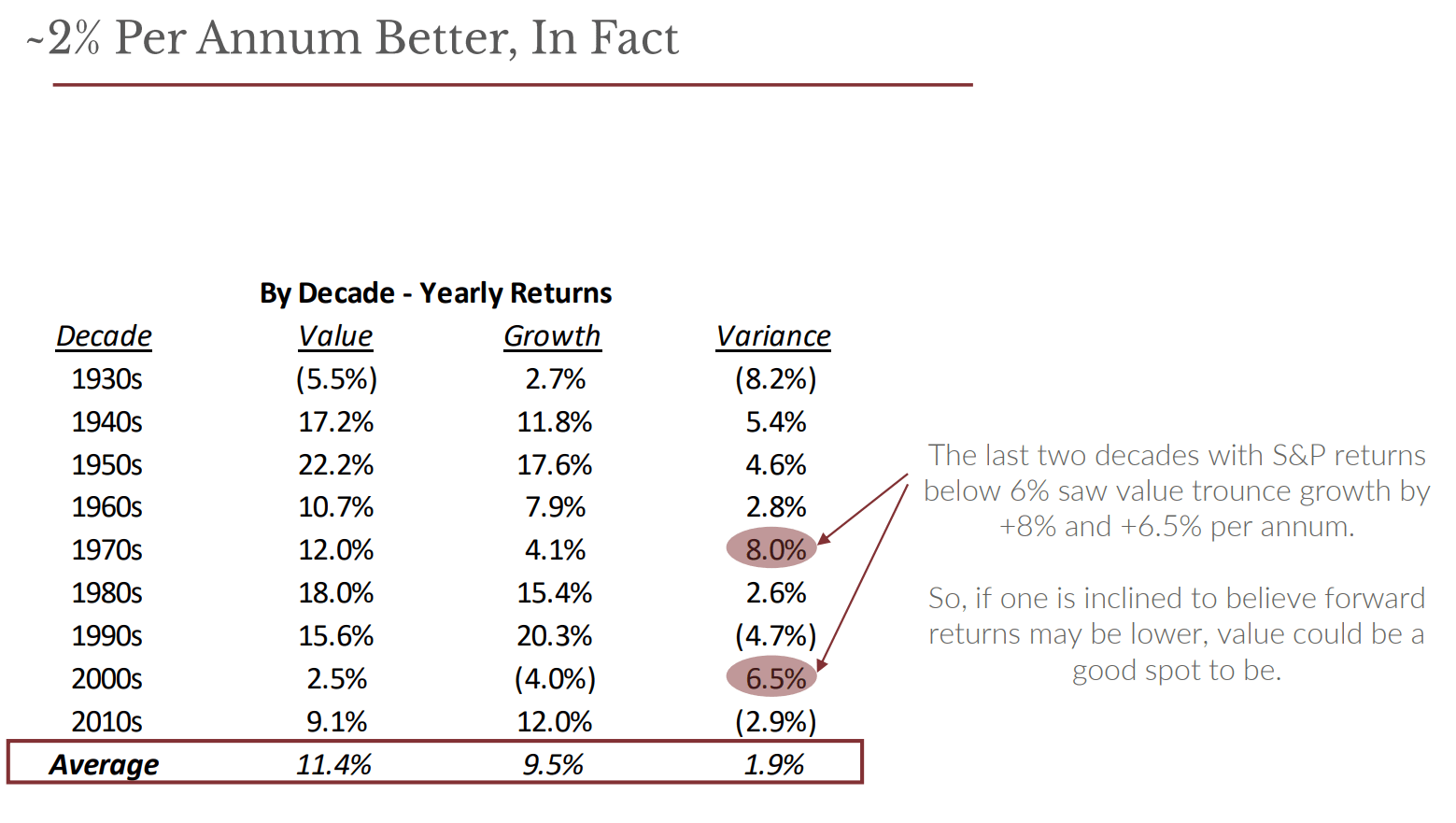

If you feel growth stocks have lately outperformed your value holdings, you are correct. Value has done well since 2010, with 9.1% average annual returns. But growth stocks returned an average 12.0%.

Over the long-term, however, value stocks typically are the MVP. Value stocks have posted an 11.4% average annual return since the 1930s, while growth stocks returned 9.5%.

Data sourced from Bloomberg.

And in the last two decades when annual returns were low — below 6% for stocks as a whole — value trounces growth. In the 1970s, when average annual returns were below 6%, value stocks did 12% while growth managed just 4.1%. In the 2000s, a very flat decade, growth stocks lost 4%, while value shares posted 2.5% net positive performance per year.

I bring this up for the following reasons.

- Don’t worry if you missed out on the big growth of the FAANG stocks (Facebook, Amazon, Apple, Netflix, Google) over the past decade. So long as you stayed invested in the market, you likely still did well.

- Yes, growth stocks have outperformed value shares in the past decade. But that doesn’t mean that growth will continue to over-perform.

- Stock returns could ease off their current 12% over the next decade. If that happens, mature companies – dividend payers with value stocks –might outpace their growth brethren.

Data sourced from Bloomberg.

So, my advice to dividend investors and value seekers is to be patient. Don’t start second-guessing yourself. Stick to what you know and believe. Your time and consistency in the market are what matters most.

This information is provided to you as a resource for educational purposes and as an example only and is not to be considered investment advice or recommendation or an endorsement of any particular security. Investing involves risk, including the possible loss of principal. There is no guarantee offered that investment return, yield, or performance will be achieved. There will be periods of performance fluctuations, including periods of negative returns and periods where dividends will not be paid. Past performance is not indicative of future results when considering any investment vehicle. The mention of any specific security is provided for illustration purposes only and should not be inferred that Capital Investment Advisors invests in the security. Additionally, the mention of any specific security is not to infer investment success of the security or of any portfolio. It is not known whether any investor holding the mentioned securities has achieved their investment goals or experienced appreciation of their portfolio. This information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors. This information is not intended to, and should not, form a primary basis for any investment decision that you may make. Always consult your own legal, tax, or investment advisor before making any investment/tax/estate/financial planning considerations or decisions.

1 Comment