What if I told you there’s a way to set your retirement asset allocation on autopilot? Would you like that idea? Or, would you think it’s probably a riskier alternative to traditional investing?

As it turns out, there is a way to automate your portfolio. It’s called a Target Date Fund (TDF). If you’ve heard of them, I wouldn’t be surprised. Right now, the estimate is that $4.0 trillion (yep, that’s a “T”) of TDFs have made their way into retirement accounts.

The number is staggering! And so are some of the downsides of this “single fund for life” investment strategy.

A Target Date Fund offers a collective approach to investing. You may have one that’s made up of a mutual fund and another by a trust fund. The aim is the same – to give investors a simplified portfolio. One benefit that proponents of TDFs tout is that 401(k) holders don’t have to choose several investment vehicles. Instead, they pick one.

With TDFs, your asset allocation changes as the “target date” approaches. This date is the day you retire, and as you make your way there, your investments are on a “glide path” from more aggressive holdings to more conservative ones.

First introduced in the 1990s, TDFs have gained in popularity in recent years because they offer a lifelong, managed investment strategy. The idea is that you can put money into your nest egg and forget about it until it’s time to retire.

But is that a good idea?

My opinion is that there is no one-size-fits-all approach to investing. And TDFs try to be just that.

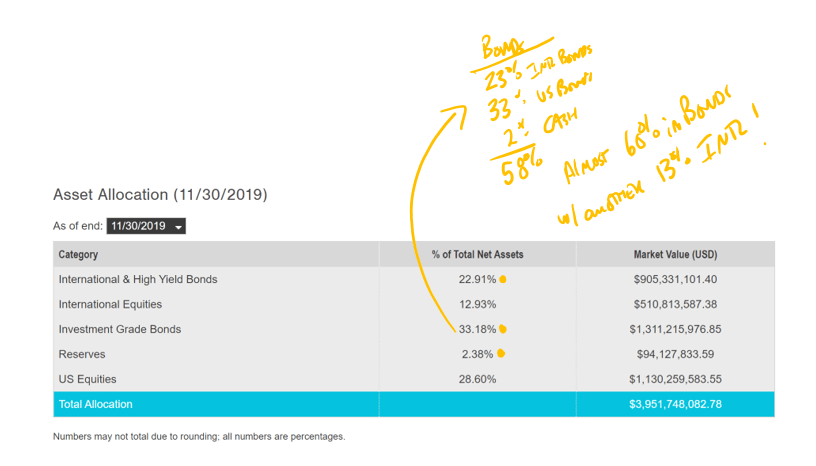

The facts don’t help the case for TDFs, either. As but one example, a TDF that has gone down the “glide path” into an allocation of 60% in bonds won’t help your retirement money last for 20 or 30 years. At least, not according to the 4% Rule.

The way I see it is that the trillions of dollars in TDFs are either too conservative or overly invested in international stocks (we’re talking upwards of 30% exposure in some cases). And these stocks have underperformed for over a decade!

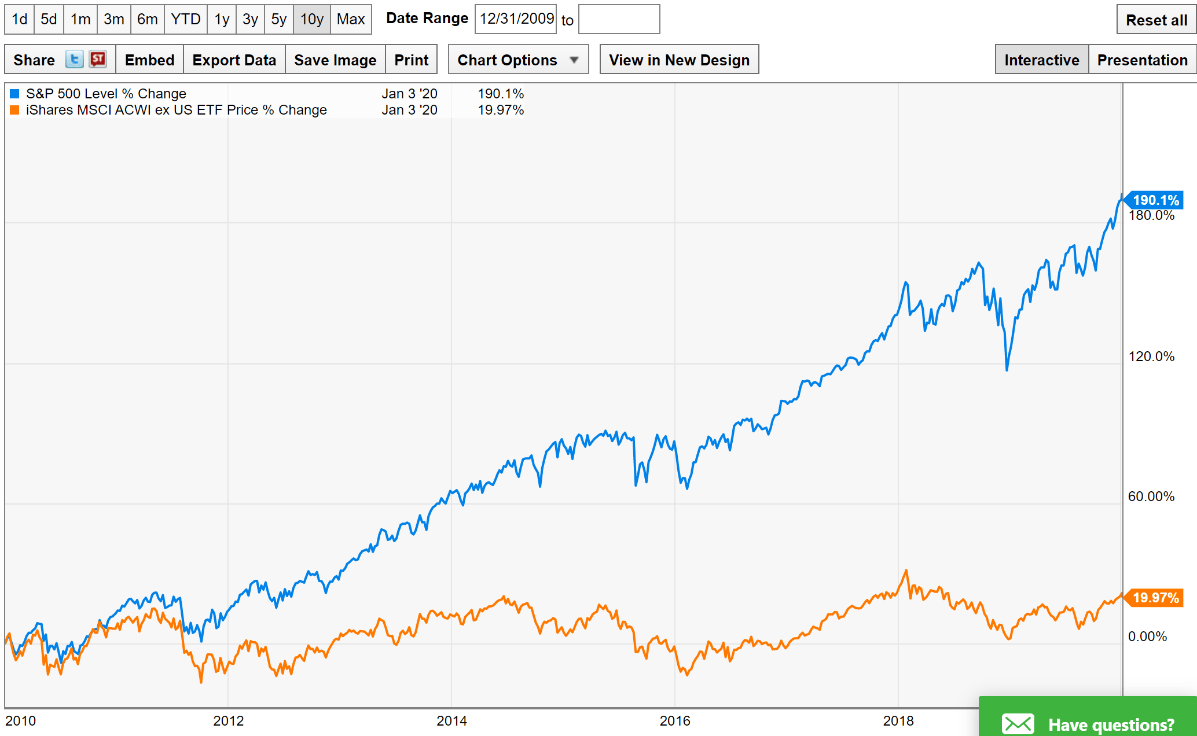

Case in point, over the last decade, the S&P 500 ended up about 190%. But the ACWX (which, in a nutshell, tracks an index composed of large- and mid-capitalization non-U.S. equities) was up only 20%. Now that, my friends, is a tremendous difference. Take a look at the chart below for a visual.

Source: Yahoo Charts

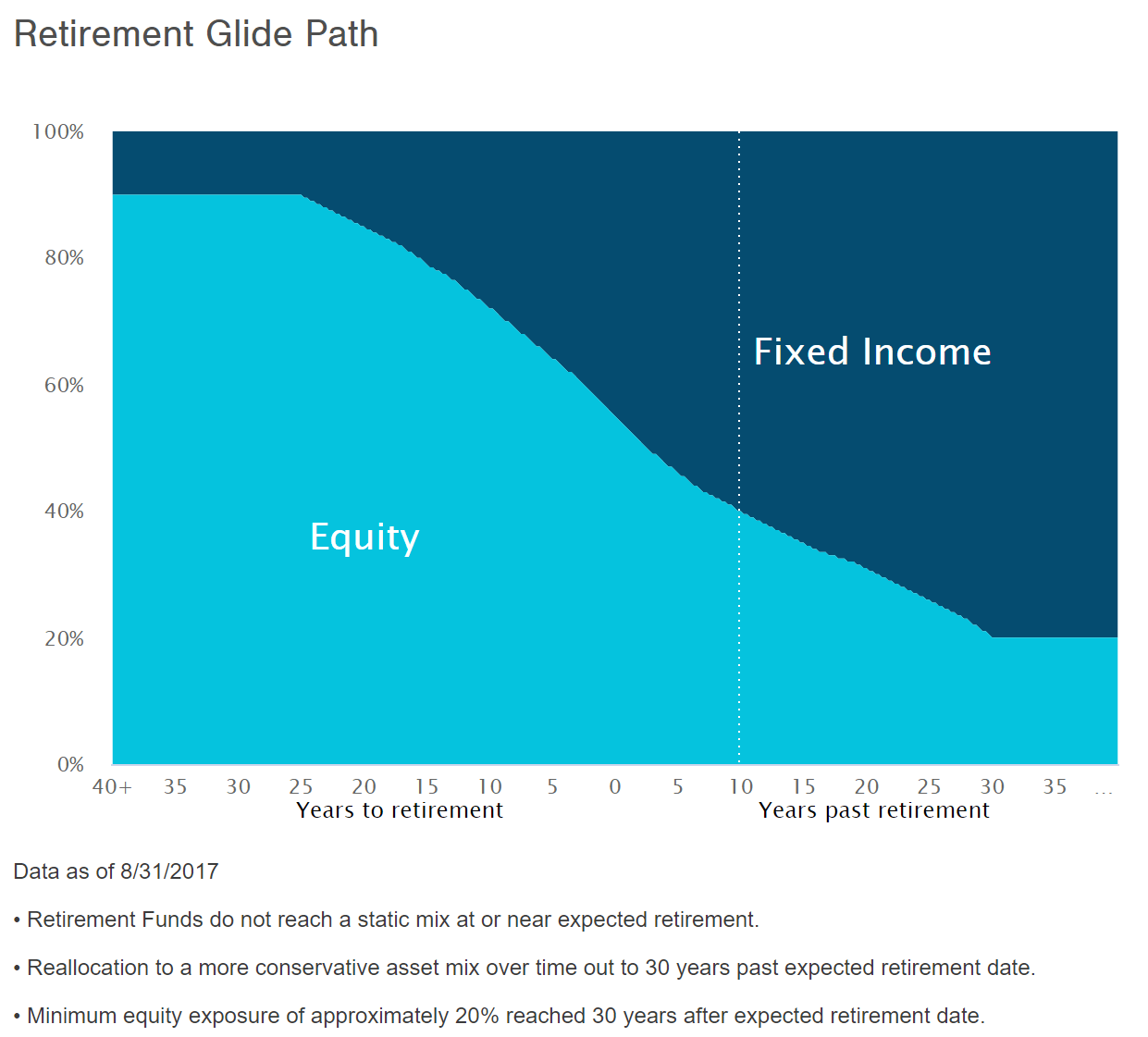

Take the below examples of the “glide path.” When you’re age 70, would you really want almost 60% in bonds? How about nearly 15% in international funds, with just above 25% in US stocks? I’m guessing your answer is no. That would be my answer, too.

Source: T. Rowe Price

Source: T. Rowe Price

I think TDFs could be a slow-moving train wreck. Think of the situation of the billions of dollars in pension funds that were governed by variables that meant well but were just wrong.

Here we have trillions in TDFs, which are a good idea on paper to give folks some balance and get them invested. But it may makes zero sense when it comes to matching up the investor’s longevity with their need for income. While 70 may be the algorithm’s life expectance, 80 or older is what we see today in real life. And, TDFs fail the 4% Rule’s (plus inflation) withdrawal rate. This rule is highly unlikely to be supported by a 60, 70, or 80% allocation to bonds and cash. And what about dividend income? Where’s that in TDFs?

Beware of the formula that TDFs may trap you in. Investing for decades should be more personalized than a set-it-and-forget-it strategy, especially when your savings journey may last half a century.

I’ll leave you with my two-word bottom line: buyer beware.

1 Comment